Reading time: 5,252 words, 20 pages, 13 to 21 minutes.

A ‘Perfect Storm’ of demography and debt will economically and financially doom almost every country on earth. It will be TEOTWAWKI – ‘The End Of The World As We Know It’.

No, it’s not the end of life or even the end of civilization. However, when it’s all over, nothing will ever be the same and that includes the disappearance of much of the middle class.

On the other hand, as Jesse of ‘Le Cafe Americain’ writes “there is nothing we are facing or are likely to face, outside of an all out nuclear war, that was not faced by our fathers and grandfathers who faced two World Wars and a Great Depression in between.” Although nuclear war is highly unlikely, the alternatives are not very enticing prospects.

First, the good news. The storm won’t last forever. In fact, it may end sooner than many think. And, when it’s finished, life for many may be better than today’s slow economic strangulation, at least for those who stop self-medicating with their boob-tubes, Tweets, iGadgets and self-aggrandizing social media long enough to pay some serious attention and try to understand what’s happening.

The bad news is there will be much more pain before it ends unless you make an effort to understand what’s happening and why. Only then will you know how to protect yourself and loved ones from the storm. Otherwise, you risk becoming just another poor, nameless statistic. That would be both tragic and unnecessary because you can do things to prepare and avoid the worst of it. Keep reading. This is a long article, but what’s your life worth?

.

Stupid Government

Governments and their handmaidens, the ass media, are trying to convince a dumbed-down, gullible public that we are recovering from the Global Financial Crisis; that they know what they’re doing and they can be trusted. Don’t believe it. Those neo-Keynesian idiots haven’t a clue what they’re doing and they can’t be trusted to run a lemonade stand let alone look out for your best interests.

Here’s but one of numerous articles titled, “Economic Bounceback Anticipated for 2014”. First, never trust forecasts. Second, it predicts happy days just as soon as the weather gets better. The Amerikan administration used to blame Bush, but that got stale so now it’s the weather’s fault. And, when that too, gets lame, rest assured they’ll dream up another excuse.

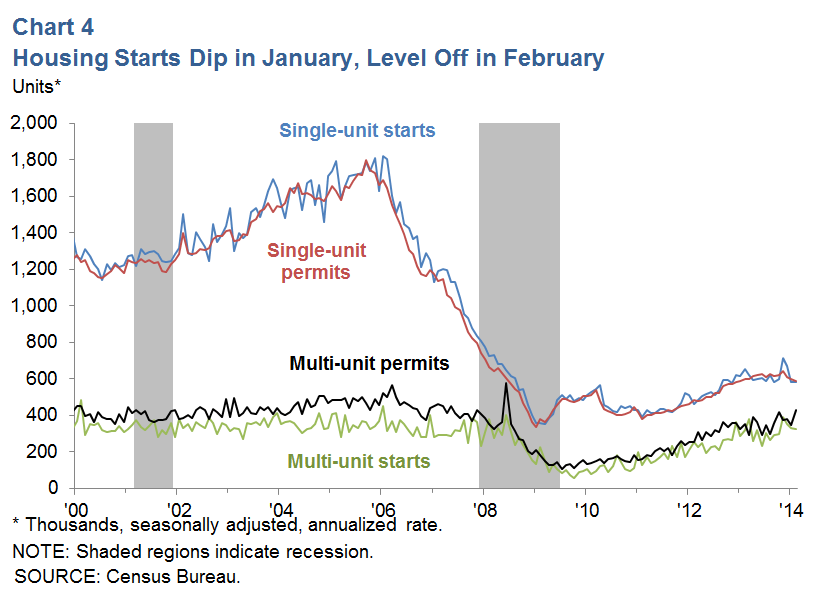

The chart below tries to spin a U.S. housing recovery. It’s titled, “Housing Starts Dip in January, Level off in February”. That so-called ‘leveling off’ is the tiny horizontal blue line on the extreme right of the chart. It’s so small it’s almost hidden by the red ‘averaging’ line.

Click chart to enlarge

Now cast your eye over the last 14 years back to 2000 and see how low today’s U.S. housing starts are compared to the last 14 years. So, who ya gonna believe; that bullshit headline or your own lyin’ eyes? Such is the ass media’s utter contempt for the public that they think we’re gullible enough to believe the crap they fling at us.

Furthermore, what little recovery there is in U.S. real estate is Wall Street snapping up homes to turn them into rental units. Some housing recovery! Canada’s real estate bubble hasn’t burst yet, but it’s coming.

Financial crises take a long time to play out and recover. How long? MoneyNews reports “The weakness of the recovery stems in part from the usual lingering hangover from financial crises, according to research by Harvard’s Reinhart and Rogoff. Their research shows that it takes a decade to fully heal … A decade is a long time. But a long time is not the same as forever.”

It also depends on how stupid governments are. As a political science major who has watched events unfold for many decades, I can assure you that no creature on earth is as stupid as a meddling government although unions come in a close second. (Disclosure: I once was a union member.)

Governments’ brainless bureaucrats lack the balls to proactively prevent problems because that would entail sticking their heads out and risk getting them chopped off. So, instead, they wait for problems to arise. Governments are reactive not proactive.

Furthermore, instead of determining the root cause of a problem (usually the government itself through its moronic meddling) they, instead, try to solve the results of a problem rather than the problem itself. You can fix problems; you cannot fix the results of a problem without creating ever more problems.

I’m also trained in the 6 Sigma continuous improvement program. One of the most powerful weapons in 6 Sigma’s ‘tool kit’ is DMAIC, an acronym that stand for Determine, Measure, Analyze, Improve and Control. With DMAIC, data and statistics are used to (first step) ‘Determine’ the root cause of a problem through measurement and analysis. Once the root cause is determined (admittedly easier said than done) only then can a process be improved. Like any recipe, if you don’t follow the steps in the right order, the results are disastrous just as baking a cake’s ingredients before mixing them will produce a mess, not a cake.

Governments’ brainless bureaucrats cannot understand this. They jump to conclusions about the cause of a problem and they almost always try to fix results. This inevitably creates more problems for the government to pretend to fix and to justify their existence. As I said, you cannot fix results. You can only fix problems and you cannot fix a problem if you don’t first determine its root cause.

For example, unemployment is a problem, isn’t it? No, actually, it’s not. Unemployment is the result of a problem so there is no ‘solution’ to unemployment unless the root cause of unemployment is determined and ‘Improved’.

President Obama recently launched the “Skills for America’s Future” program to “improve industry partnerships with community colleges and build a nation-wide network to maximize workforce development strategies, job training programs, and job placement.”

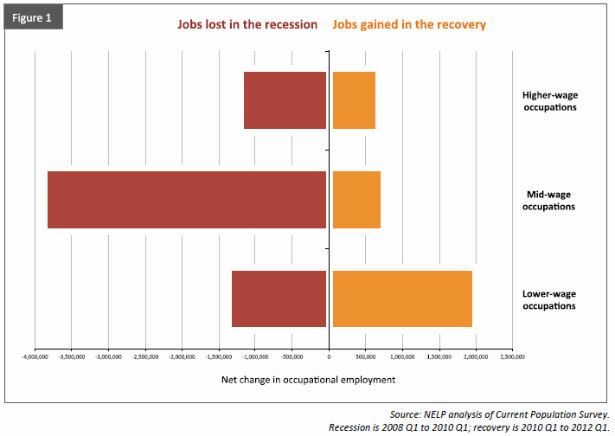

That sounds wonderful. However, contrary to popular belief, governments do not create jobs. Government meddling and over-regulation destroys jobs. What’s the point of training people for jobs that have been moved overseas? Well-paying jobs in manufacturing have been replaced with low-wage McJobs. The chart below shows low-wage jobs replacing mid-wage and high-wage jobs.

Notice above how most of the jobs lost are in the mid-range.

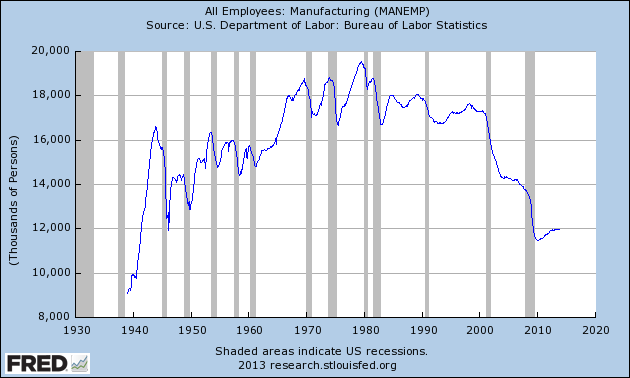

The chart below shows how much high-wage U.S. manufacturing has declined since 1980.

Again, the problem is not unemployment; the problem is lack of well-paying jobs caused by outsourcing and by corporations’ short-sighted fixation on short-term profits thereby destroying their own customer base. In other words, more training won’t fix the jobs ‘problem’.

.

Problems Getting Worse

Inept governments have done nothing to fix the issues that created the Great Financial Crisis and the resulting recession. My previous article demonstrated we are overdue for another recession. This is also confirmed by Yahoo! as well as the National Bureau of Economic Research (NBER) and various other articles.

Since the problems that caused the last recession have gotten worse, the next recession will be more…painful than the last one despite so-called GDP growth.

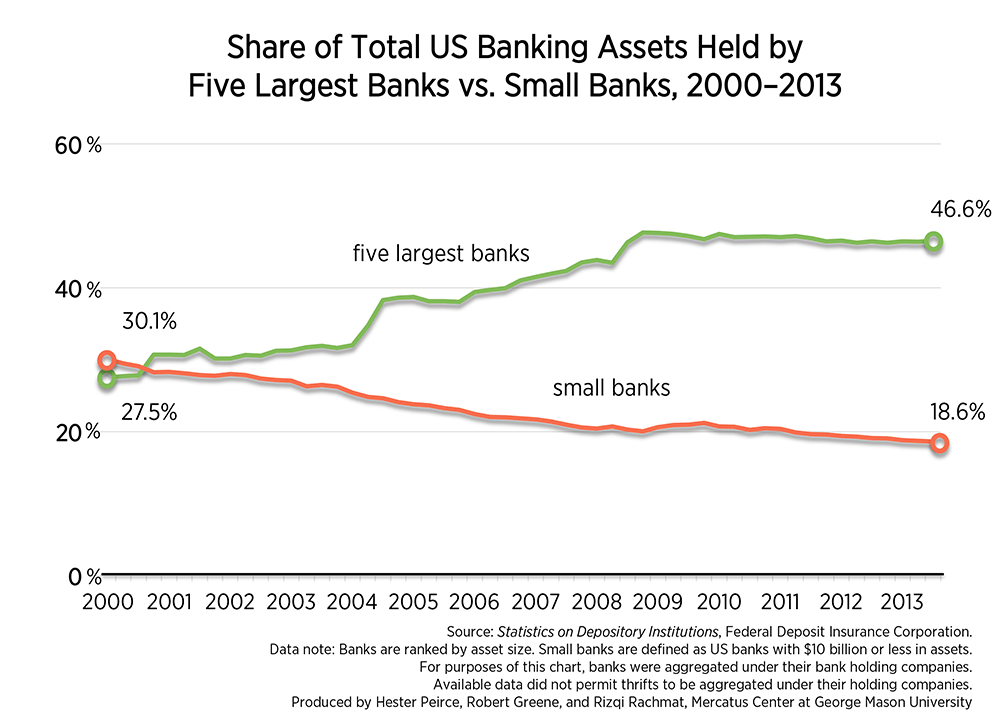

For instance, the Too-Big-to-Fail banks have gotten larger than before thereby putting them at greater risk. National Review reports that since the year 2000, there are 29% more big U.S. banks and 24% fewer small ones as shown by the chart below.

Not only are banks larger, but world-wide most banks, including central banks too, are insolvent (bankrupt) and starting to panic.

Another indication of a slowdown is the closing of so many retail stores. Even MacDonald’s is feeling the pain. In addition, inflation, especially in food, is getting worse which will further impact cash-strapped consumers.

I’ve outlined numerous other problems that have been ignored rather than solved in many previous articles so there’s no point repeating them ad nauseum.

.

It’s the Debt, Stupid

The single, major global problem is too much debt. Much of the commentary and analysis I read is misguided. Everyone’s talking about the consequences (results) of the problem yet few understand that the elephant in the room is too much debt.

Global debt has passed the $100 trillion mark, an increase of $30 trillion since 2007. To put this into perspective, global GDP is slightly more than $70 trillion. Here’s another perspective; global debt is 137% of global GDP. This is far beyond the 90% mark demonstrated by Rogoff and Reinhart (despite a few minor formula errors) as ‘beyond-the-point-of-no-return’.

The last Great Recession triggered by the Global Financial Crisis was caused by too much debt – private debt, government debt, corporate debt, Sesame Street debt, all kinds of debt – we have debt up the yin yang and it keeps growing.

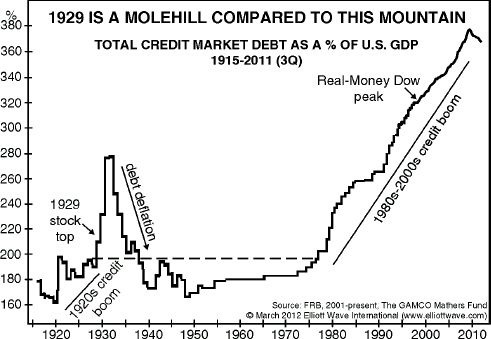

The chart below shows that today’s mountainous debt level makes the debt prior to the last Great Depression look like a molehill. The debt/credit excesses of the 1920’s led up to the stock market Crash of 1929 and the Great Depression that followed. Can there be any doubt where today’s enormous debt level is leading?

Some of Aubie Baultin’s comments on the chart above are instructive:

“By 1982, with the memory of the 1930s Depression almost completely faded, policy makers once again began to “stimulate” the economy with borrowed dollars. By the mid-1990s we had exceeded the excesses of 1929 both in terms of the total amount of debt and in terms of stock prices.”

“As of 2014; there is currently 30% more debt worldwide than at the last peak in 2007 and we are experiencing one of the weakest recoveries of all time.”

“The bubble is much bigger than in 1929, [when] we as a people were much more self- sufficient and so the economic destruction will be worse damaging to the individual than in the 1930s!”

“We may have engineered a very anemic recovery and new highs in the stock market, but we haven’t solved the underlying problem of too much debt. Rather, we have made it much, much worse and that’s not even mentioning Derivatives in the Quadrillions.”

“When the boom ends, the accumulated debts do not.”

“A year before the 1929 crash, interest rates started rising while commodity prices fell indicating a risk of deflation – or collapse in prices. The same scenario is true today.”

“[China is] are probably in the worst trouble of all, as they discover that their Socialist Capitalism must still follow the Economic laws …”

“There isn’t a snowball’s chance in Hell that we will be spared the consequences of our leaders’ incompetence and corruption.”

I’ve already covered government’s incredible incompetence, but the corruption is all the new debt that has benefited the banksters and their cronies, but not the people. It has enriched Wall Street by impoverishing Main Street. Worse, as headlined by Washington’s blog, “By Choosing The Big Banks Over The Little Guy, The Government Is Dooming BOTH.” He further headlines “The Elite Financial Players Are Manipulating the Game So that They Get the Stimulus … and the Little Guy Gets the Austerity.”

Do you think this will ever stop? Dream on. The great ‘Vampire Squid’ will suck every drop of blood out of the system that it can. To protect yourself you must ‘Get Out of The System’ or GOTS as Jim Sinclair says.

Here is his GOTS checklist for those with wealth to protect.

1. Your equities are held in certificate form. [Gerold comment: paper stock certificates]

2. You have no Federal retirement funds. [Gerold comment: expect governments to confiscate pensions and turn them in to soon-to-be worthless government bonds. Cash out private pensions, take the tax hit and buy assets with the cash.]

3. You have no CDs and investments in bonds. [GIC’s in Canada]

4. You have modest money deposited among selected BRICs countries.

5. You store your own precious metals. [gold & silver]

6. You have no mortgage obligations.

7. You keep cash on hand for 6 months expenses.

8. You have no consumer debt at all.

9. You have a small hobby farm for protein and veggies outside of where you are living with no mortgage debt, set up green.

10. You have a gas, diesel or electric car with high fuel mileage for the farm.

11. You have a generator with large fuel capacity for the farm.

It’s not easy but the more you remain in the system, the more vulnerable you are to further losses, bail-ins and pension confiscation.

.

The Power of Demography

Demography (sometimes called demographics) is the statistical study of human population dynamics over time or space. The characteristics of a population include size, structure, density, distribution of the population and the changes resulting from birth, migration, aging, and death. Demographics is as powerful as it sounds and it has enormous predictive abilities.

One of the most powerful demographic cohorts in recent times has been the Baby Boom generation. Michael Snyder writes “The Baby Boomer generation is so massive that it has fundamentally changed America with each stage that it has gone through. When the Baby Boomers were young, sales of diapers and toys absolutely skyrocketed. When they became young adults, they pioneered social changes that permanently altered our society.” And, it’s not just Amerika affected by these demographics but most Western nations including Canada, Great Britain, Australia, New Zealand, much of Europe, etc.

Demography can forecast trends and patterns years and decades in advance. New York Post reports “Following the Baby Boom, which peaked in 1961, came the Baby Bust, a long slow decline in the birthrate. Those babies grew up and began spending in accordance with highly predictable patterns.

“People tend, for instance, to buy houses at about the same age — age 31 or so. Around age 53 is when people tend to buy their luxury cars — after the kids have finished college, before old age sets in. Demographics can even tell us when your household spending on potato chips is likely to peak — when the head of it is about 42.

“Ultimately the size of the US economy is simply the total of what we’re all spending. Overall household spending hits a high when we’re about 46. So the peak of the Baby Boom (1961) plus 46 suggests that a high point in the US economy should be about 2007, with a long, slow decline to follow for years to come.” And, that is exactly what happened; Western economies began their decline around 2007 with the recession beginning in the U.S. in December of that year followed shortly after in other Western countries.

In the birth-rate chart below, the Baby Boom is the red portion of the line that interrupted the gentle decline of birth rates.

There is much demographic tragedy on the left side of that chart. The high birth-rate in the early part of the 20th Century is due to high infant mortality. Families had many children because most weren’t expected to survive their early years. Also, the rapidly declining birth-rate after the First World War 1914 – 1918 comes from the unmarried “surplus women”

as a result of the war slaughtering so many “eligible” young men.

Japan is another case of obvious demographic trends that still eludes their government’s understanding. The New York Post quotes Harry S. Dent Jr. in “The Demographic Cliff: How to Survive and Prosper During the Great Deflation of 2014-2019” (Portfolio), “Japan’s stock market is still 65% below its 1989 peak. Their spending problem (currently being given a boost by a gigantic stimulus) is really … an aging problem.

“As the Japanese have hit their 60s and 70s, they became stingier. Artificial, forced spending like government stimulus is not going to spark real voluntary spending because that isn’t what old people do. They’ve already paid for their houses, cars and their children’s schooling. Merchants try to goose lackluster sales by cutting prices, which increases the incentive for people to save their money, expecting things will be cheaper in the future than they are today.

“That’s a deflationary spiral, and Dent sees it coming here next, and soon.” In other words, we will soon see that Japan’s massive QE, called “Abenomics”, is a greater disaster than America’s endless rounds of QE which failed to spur the U.S. into a real recovery. In the U.S. it’s sometimes called a ‘jobless recovery’. That’s nonsense. Even disregarding the Amerikan government’s fake unemployment statistics, a real recovery in jobs never happened because the economy never really recovered.

Stay tuned to China, too. We will soon see the disastrous effects of the massive Chinese QE of infrastructure spending and the construction of ‘ghost’ malls, rail stations and empty cities which proportionately dwarfed the U.S.’s QE. The Chinese defaults are already beginning. China’s demographic problems are unique; stemming from its decades-long ‘one-child’ policy resulting in a ‘Baby Bust’ far larger than the West’s.

.

The Greying of the West

The Financial Times reports “The drop in the percentage of Americans at work in recent years is often cast as a story about the long-term unemployed who give up trying to find jobs.

“But the declining workforce participation rates, which have sharply reduced headline unemployment calculations in the world’s largest economy, could be related to a very different phenomenon: the greying of America.

“What is more, the trend is set to continue until around 2020 regardless of how the economy fares.” And, it’s not just the greying of America but most Western countries as well.

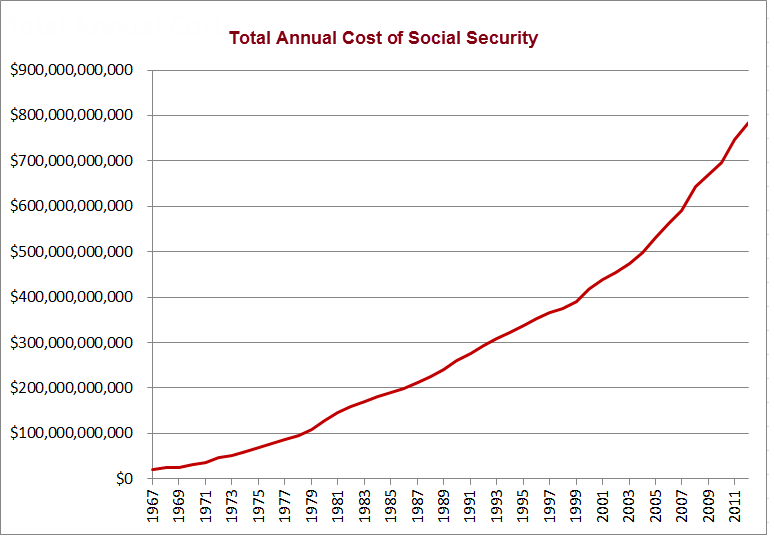

The jobless statistics are improving, but with more and more Boomers retiring the economy is impacted with fewer workers, less spending, less tax revenue thus straining the U.S. social security system and making it more politically unpalatable to fix. The chart below shows how the geometrical rise of social security cost is out of control.

Boomers are retiring from relatively well-paying jobs and leaving a larger proportion of low-wage workers in the work force resulting in even less spending and further declining tax revenues. Furthermore, unfunded pension liabilities are increasing as are health-care costs as a result of this demographic trend. Even countries like Canada which does have a funded public pension plan will also suffer greater demands on the Canadian Pension Plan (CPP). In addition, Canada’s universal health care system will be strained to accommodate this huge cohort of aging Boomers.

As you can see, demography is a very powerful force affecting us all as well as our economy and our future. It is a testament to governments’ incredible stupidity that they have never understood the power of demographics nor have they been able to plan according to these very obvious demographic trends.

For example, forty years ago when the Baby Boom’s bulge in our population was reaching high schools there was inadequate classroom space to accommodate the increased student population. My high school went on a double shift with half the students going to school on the first shift in the early morning and the other half on the afternoon shift.

It’s not as though school boards and education departments couldn’t see it coming. High-school student didn’t just miraculously drop out of the sky. High school students came up through the primary grades. Administrators knew there was an increase in primary grade students, yet they failed to grasp that most primary grade students would go on to high school. Were they expecting that students would somehow disappear off the face of the earth?

Demographics also would have told them that they had built too many primary grade schools and many of these classrooms were no longer needed once the Baby Boom bulge had passed through. Administrators failed to anticipate this and did not plan for the gradual closure and consolidation of schools. Instead they waited until schools were half empty and then, with short notice, they began closing schools en masse. Needless to say, this enraged parents, many of whom would lose their neighbourhood schools. Never underestimate the power of government incompetence.

It is a testament to the incredible incompetence of governments’ brainless bureaucrats that they are incapable of learning from their past mistakes. Today, governments still don’t have their arms around demographics as we’ll see below.

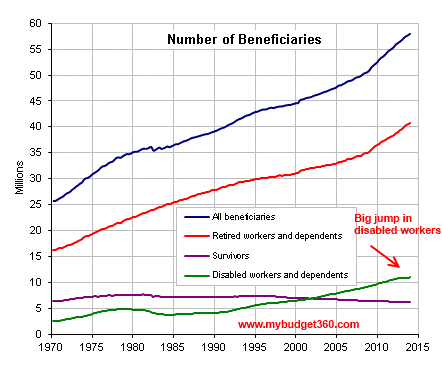

Nowadays, 10,000 Amerikan and 1,000 Canadian Baby Boomers are retiring every day. That’s every DAY! It should come as no surprise that governments are inadequately prepared to sustain this social security safety net for very long.

For example, since 2000, the U.S. population has increased 13%. As seen in the graph above, the social security beneficiaries have increased 28% and those on disability 100%. This is simply not sustainable yet nothing is being done about it.

Furthermore, most social security safety nets require a constant stream of funding from current workers which means a young workforce. However, many of the young are already burdened with a with a triple whammy:

1)They are working in low-wage jobs.

2) They are saddled with massive student debt.

3)They are paying much higher social security taxes than previous generations and yet they’ll see fewer benefits.

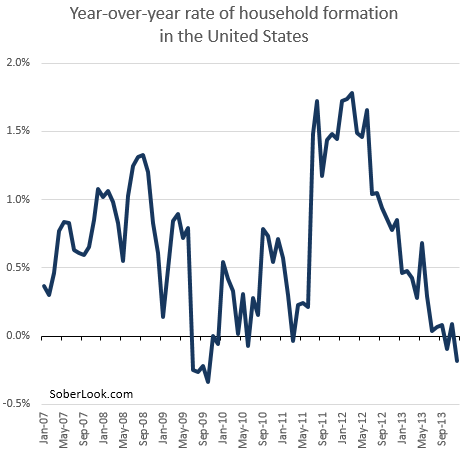

The impact on the young can be seen in the graph below on ‘household formation’ where the young can’t afford to ‘leave the nest’ so more and more are living in Mom’s basement.

MyBudget360 reports “You have more people living at home between the ages of 18 and 31 than you did during the Great Depression!”

.

Unprepared for Retirement

A large number of Boomers are financially unprepared for retirement. They are working longer and their retirement age keeps increasing.

Boomers’ delayed retirement denies younger generations jobs and experience which will also have long-term negative impacts on the economy.

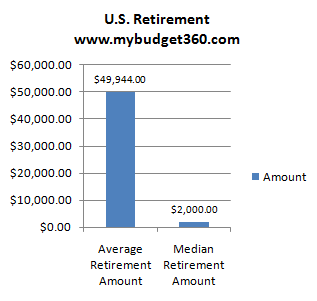

The graph below illustrates how unprepared Amerikan Boomers are. Notice the large discrepancy between ‘Average Retirement Amount’ on the left and “Median Retirement Account’ on the right.

MyBudget360 explains this as, “The average is a poor metric because it takes into account the few outliers with millions. The median shows us where half of people fall below and above and the picture isn’t pretty.”

“Since we have a massive cohort of Americans entering retirement age everyday having decades ahead to right the ship will no longer be an option.”

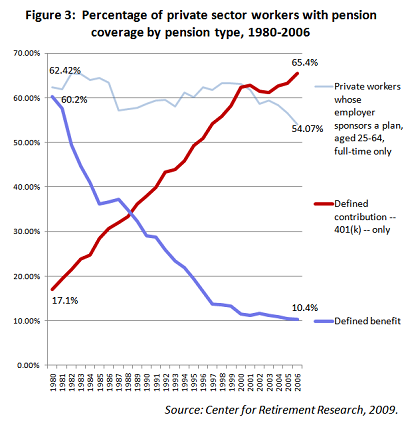

One of many reasons so few Boomers are unwilling and unprepared for retirement is the decline in defined benefit pension plans and the increase in defined contribution plans. In 1980, 60% of workers had defined benefit plans whereas today it’s fallen to 10% while the number of defined contribution plans (individual responsibility) has increased from less than 20% to well over 60% as shown in the graph below.

With defined benefit plans (“divine” benefit) the company would top-up any shortfall in the plan. With defined contribution plans, the individual was solely responsible. The graph above shows the defined benefits as the descending blue line and the rising red line is defined contributions.

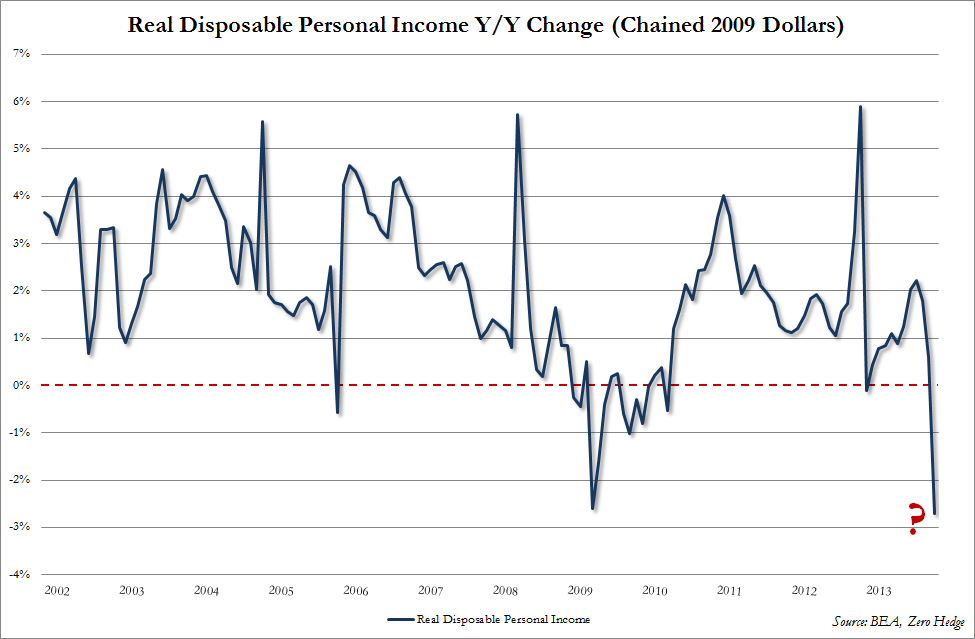

With stagnant…incomes more people are living hand-to-mouth and unable to save.

As you can see from the chart above, the trend is clearly downwards.

Tyler Durden of Zero Hedge says, “We may not know much about “Keynesian economics” (and neither does anyone else: they just plug and pray, literally), but we know one thing: when real disposable personal income drops by 0.2% from a month earlier, and plummets by 2.7% from a year ago, the biggest collapse since the semi-depression in 1974, something is wrong with the US consumer.” And, with central banks’ Zero Interest Rate Policies (ZIRP), those who could actually save earn practically nothing in interest.

CBS reports “roughly half of U.S. families don’t have a single dime set aside for retirement.”

Many people find it, “hard or impossible to save because of their precarious situations — unemployment, stagnant income, impossible health costs or other factors.”

“… perhaps the biggest obstacle to saving for retirement in the United States is that wages for nearly all Americans have been stagnant for more than 30 years — a trend that has continued following the housing crash and the weakest post-recession recovery in U.S. history.”

MoneyNews reports, “There are no documented examples of an economy that had to emerge from a financial crisis while simultaneously absorbing the effects of an aging population, noted Harvard University economist Carmen Reinhart, who has researched eight centuries of crises with her colleague Ken Rogoff.” In other words, the situation is far worse than we realize.

.

Depression May End in 2020?

Many believe the recession/depression began about 2007 (myself included) but there’s considerable evidence to think it started even earlier. Many signs point to the year 2000. Jim Quinn of the Burning Platform calls this the “Fourteen Year Recession” that began with the bursting of the DotCom bubble.

We’ll have to wait for future historians to cast their vote. If this is a typical Depression and it began in the year 2000 and Depressions last an average of twenty years then 2020 (the anticipated “reset”) may see us clawing our way out of it. That’s, of course, assuming this is a typical Depression and not the ‘new normal’. Only time will tell. In either case, it’s wise to prepare as outlined below and in my previous survival articles.

.

Investment Suggestions

In a slower growth world with ageing demographics, an investor needs to think outside the box used by his grandparents or even his parents by focusing on yields or dividends rather than equity appreciation (rising stock prices). This also means educating yourself in investing and not relying on traditional ‘buy and hold’ techniques.

An investor must be prepared to change investment strategies as resource and commodity prices change. This means paying a lot more attention and being nimble. It also means going against the herd (nothing new there).

Our owners, as George Carlin called them, will continue blowing asset bubbles for their cronies that can be profitable for investors mentally prepared to buy when fear is greatest and sell when euphoria is highest (not new, either but mentally difficult). Also, consider stocks in companies more likely to improve productivity rather than those that rely on an ever-expanding customer base.

Some of the most important investment lessons I’ve learned the hard way are:

1) Patience.

2) Don’t be afraid to sit on the sidelines because you don’t need to be fully invested all the time.

3) Small losses are better than hope because that can result in larger losses. Hope is not a plan.

4) Ignore the daily noise. Stock markets fluctuate and the reasons given by the ‘talking heads’ is meaningless babble.

5) Ignore ‘hot tips’. Educate yourself and make your own decisions.

6) For lots more, see my hard-earned stock investing lessons.

James Gruber suggests, “investment opportunities in areas which provide solutions to some of problems of ageing demographics and resource constraints. Robotics to improve work productivity, for example. Biotech to help us live (and work) longer. Healthcare technology which helps mitigate rising healthcare spending. And in agriculture and renewable energy as resources constraints become more urgent.”

.

Social Warfare – Divide & Conquer

Demography lends itself to generational and social warfare as our ‘owners’ and their ass media minions encourage groups and generations to fight and flame and blame each other rather than the real enemy. Republicans fight their own Tea Party, Democrats fight Occupy Wall Street, the young blame the old, the old disparage the young, liberals blame conservatives and on it goes.

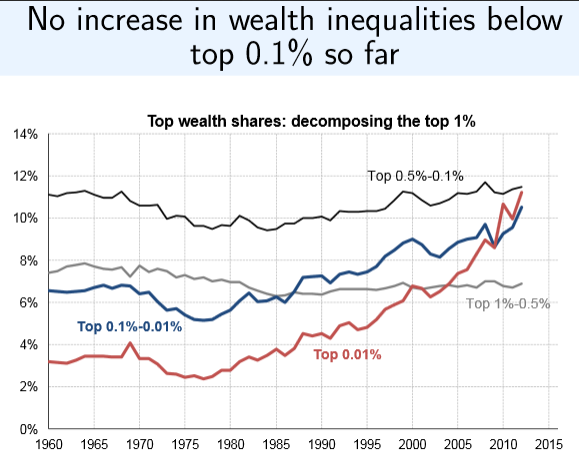

We hear much about the ‘top 1%’ getting wealthier at the expense of poor little us, but that too is part of our owners’ divide & conquer strategy. It looks increasingly like the top 1% are being positioned as the next patsies to be fleeced by desperate governments. Meanwhile, they make convenient targets for our hatred and to distract us from real issues. It’s not the top 1% or even the top 0.1% whose wealth is increasing, but the top 0.01% as per the chart below.

Note that this chart tracks percentage not nominal dollars. It’s only the top 0.01% (red line) whose percentage of wealth is increasing. Those are our ‘owners’, not the banksters; they’re just the bag men. It’s not the Warren Buffets or George Soros of the world; those are just the front men. It’s the nameless and faceless few families who are never seen in public that control the puppet strings to which we all dance and, the more indebted we are, the harder we dance.

Yet we blame everyone else. We blame immigrants who generally aren’t afraid to work hard and show up the rest of us. We blame Muslims, the Jews, etc. We blame everybody except ourselves. When we point a finger, we conveniently forget that there are three fingers pointing back at ourselves. Never underestimate our incredible ability to avoid accepting responsibility for ourselves.

So much for the land of the ‘free and the brave’ who have allowed themselves to become a dumbed-down, self-medicated, digitally-addicted nation of sheep coerced by uniformed thugs and governed by corrupt, paid-for leaders. That’s why I spell Amerika with a ‘K’ rather a ‘C’ in memory of a nation that has willingly surrendered its freedom for the illusion of security and received neither.

.

The Real Enemy

The real enemy is both ignorance and debt and especially the ignorance of the pernicious effect of debt in creating debt-slaves that elect politicians that support a central bank-controlled financial system of usury and inflation that robs us of the purchasing power of money. Once you understand that, you can prepare and avoid the worst of the storm.

.

How to Prepare

– Reduce your debt, get out of debt and stay out of debt

– Keep only as much money in the bank to pay your bills and avoid future Bail-ins.

– Stay away from banks altogether. Use a Credit Union. They’re slightly safer, friendlier and easier to deal with.

– Buy assets. Depending how much money you have; if you’re wealthy, buy the company rather than its stock because stock markets crash.

– If you have medium wealth, buy cheap land (admittedly hard to find) as well as hard assets and gold.

– If you have small wealth, diversify into one ounce silver coins, long term food storage and durable necessities like toilet paper, garbage bags, etc. In other words; stockpile.

– Even if you have only a little money, there are things you can do to protect yourself and your loved ones. Educate yourself. Stop watching the boob-tube. It rots your brain. There are many alternate sources of information.

– Re-read Jim Sinclair’s GOTS checklist above.

– If you understand nothing else then understand this: money is NOT real. Money is simply an agreement, an IOU that eventually will be worth less than toilet paper. You need to copy Warren Buffet and convert your money into tangibles, real stuff, real assets that the governments cannot confiscate.

As Yogi Berra once said, “It’s tough to make predictions, especially about the future.” However, many ‘hard money’ financial analysts predict the ‘Great Levelling’ in about 2016 and the ‘Great Reset’ in about 2020. That’ll be here before you know it. The levelling will be the time of loss and confiscation. The reset will be the new currency, just like the old currency and you can bet it will be created to their advantage, not yours.

So, you must protect yourself by preparing for it as outlined above. If not, you’ll be just another statistic. It’s your life and your choice.

Remember the mantra:

We cannot borrow our way out of debt.

We cannot spend our way to prosperity.

We cannot pretend our way out of trouble.

Lord knows, they keep trying …

Gerold

April 5, 2014

Your comments are WELCOME!

If you like what you’ve read (or not) please “Rate This” below.

Lengthy comments may time-out before you’re finished so consider doing them in a Word doc first then copy and paste to “Leave a Reply” below.

Pingback: My Homepage

The real tragedy of all this is that while people in Africa die of hunger, they are “used to it”. That’s not being sarcastic, it’s a statement of fact (Let’s not forget that most of these food shortages in Africa can be attributed to the EU’s CAP or “Common Agricultural Policy” and the US’ subsidized food exports etc.). But these Westerners will not even die of starvation when their pay- or pension checks stop suddenly. They’ll be so shell-shocked they just die of depression and mass suicides. Apart from those so demented that they die in their beds in nursery homes all of a sudden deserted by those formerly helpful immigrants who now also have to see how they can feed their families after a collapse. I wonder what historians will say about the next fifty years when they write about in, say, five hundred years.

Well said, Oona. I couldn’t agree more and I’ll add one thing. What happens when a significant part of the population – I’ve read between a quarter to a third are taking prescription anti-depressants – go off their meds when supply chains break down?

You say, “They’ll be so shell-shocked they just die of depression and mass suicides.” That covers the self-inflicted deaths. What keeps me awake is that most of the recent mass murderers were on, then off these prescription anti-depressants. Now, multiply that by millions.

You can see why I want to fast forward my life twenty years. Ok, I’d even settle for ten just to avoid more of the heartbreaking shit-show by the terminally clueless, great unprepared masses.

– Gerold

Pingback: UPCOMING FINANCIAL MARKET DOOM…….. |

Thanks for contributing to the debate. Very interesting. I’ll make a point of reading your blog. My only reservation is the world is very complex. People are very motivated to succeed. There is lots of data that one can collect to make a case, but much more important elements such as innovation and adaptation cannot be quantified but have large effects. Therefore, being sure about TEOTWAWNI may prevent winning in the meantime. The point you make about being nimble is important. If there is an asset market with opporutunity, even if it lasts only six months or a year, one must try to take advantage. One friend has been waiting 10yrs to buy a house, always thinking prices were too high. Today, he is much poorer than he could have been since he failed to buy 10yrs ago.

You’re right, James, the world is indeed complex. Like peeling an onion; there’s another layer underneath.

TEOTWAWKI is not a reason to surrender. I’ve stated in previous posts that the right attitude (“never give up”) is more important than gear and skills. Markets and assets will become more volatile so we need to educate ourselves to increase our flexibility to get in an out and take advantage of the volatility. ‘Buy and hold’ doesn’t work anymore.

– Gerold

I had to stop reading when you replaced what should have been NAFTA with “the problem is lack of well-paying jobs caused by outsourcing and by corporations’ short-sighted fixation on short-term profits”.

Pingback: Demography + Debt = Doom | Exploring the World

Pingback: Guest Post: Demography + Debt = Doom

Pingback: Guest Post: Demography + Debt = Doom - UNCLE - UNCLE

Pingback: RedTrack.ME

Excellent Metaphor. Absolutely correct the Ark was built because one man had the wisdom to listen and the knowledge to understand. Thousands perished, yet right up till the moment the rains came only 8 listened out of

tens of thousands much like today

Its funny how history repeats itself, yet the illusion of having freedom does not mean the chains of slavery have ever been removed.now its just done in an overt fashion. How did anyone every forget the term Usury or better yet the Money Changers? Right in plain sight, yet the world seems to have a veil over their eyes and few will see it till its hits them in the face. People only want to hear the Roses are up and the rains have stopped.

Ken

Ken, yes indeed, people only hear what they want to hear.

Mark Twain is credited with saying, “History doesn’t repeat itself, but it does rhyme.” And Straus & Howe’s book, “The Fourth Turning” demonstrates a four generational cycle throughout history and then it’s rinse, repeat because there’s no one left or with enough power to prevent us repeating our mistakes.

The only thing we learn from history is we don’t learn from history. Sad, but true.

– Gerold

Hi, Gerold

I would like to take thank-you for all the work you place into the economic facts and provide the a clear view of what individuals should really be doing. It is on difficult days such as today that we realize our family is much better off than those with mortgages plus debt. We are in a rental and we have our difficult days as the place is for sale for a insane price and we have individuals going through weekly, yet because of you and your articles we realize all these home buyers are pretty well burying themselves into debt slavery.

as difficult as it may be as a renter I for one will be thankful the day a reset comes because there’s days if you didn’t have your head screwed on right you could go insane with what’s going on in this world. I feel like we live around a flock of sheep with their head stuck were the sun don’t shine. It is just is amazing to watch the blind leading the blind. Even without a degree I can see the real issues in this world, yet we have so called professionals that can’t present the real facts when its starring them right in the face. Is it just me or is everyone around us pretty well delusional watching the latest things happening in Hollywood?

Take Care

Ken

You’re right, Ken. We do live among a flock of sheep with their heads stuck up nether regions. The worst of it will be when the SHTF and we have to listen to their bleating and they’ll call upon the government to save them from themselves, much like the hens calling on the foxes to guard the hen house. Also, when the SHTF, they’ll call it a “Black Swan” event despite it being foreseeable.

I credit my foresight to being TV-free for 24 years although I sometimes feel like “A Stranger in a Strange Land”when dealing with the zombie sheep. However, that ‘outsider-looking-in’ perspective enables me to see the warning signs and devote my spare time to researching and writing these articles warning whoever is brave enough to see. All told, it takes one to two hours of reviewing, researching, writing, re-writing, editing and posting for every minute of one of my article’s reading time. I don’t begrudge the time I spend because I know I’m helping people (I wonder if there’s such a thing as an ‘older brother syndrome’?).

It must be heart-wrenching you seeing those future debt-slaves. I’m sure most of them are good people and yet .. and yet … I’m at a loss for words. Jim Quinn says it well, “The most highly educated zombies will be the most shocked when they realize the reality they believed was all an illusion.”

In Greek mythology, it was Cassandra’s curse to be always right but never believed. Tragically she was unable to prevent her own predicted death. Such is our fate – I mean the disbelief and hopefully not the death part.

You mention “so-called professionals that can’t present the real facts when it’s starring them right in the face.” I’m reminded that the Titanic was built by professionals, the Ark was built by an amateur. See “Normalcy Bias” https://geroldblog.com/2013/04/26/beware-your-dangerous-normalcy-bias/ to explain how even well-intentioned and intelligent people can ignore obvious danger signs. That’s only part of it. In addition to that is the pervasive propaganda that brainwashes the sheep and lulls them to sleep.

Little is known about Carthage because their enemy the Roman Empire obliterated most traces of that ancient empire. Although, the Carthagian capital was burned and levelled, the remaining Carthagians were assimilated into the Roman Empire through Rome’s all-encompassing propaganda which was crude compared to today’s very sophisticated and pervasive propaganda. If crude Roman propaganda can transform an enemy into a subdued Roman citizen then it’s no wonder that today’s sophisticated propaganda works so well on willing citizens.

– Gerold